If your bank asked for Form 121, don’t worry. Earlier we had Form 15G and 15H, but now both are merged into one form — Form 121.

This article explains Form 121 used for TDS declaration in banks and financial institutions. If you are searching for EPFO/PF Form 121, that is different.

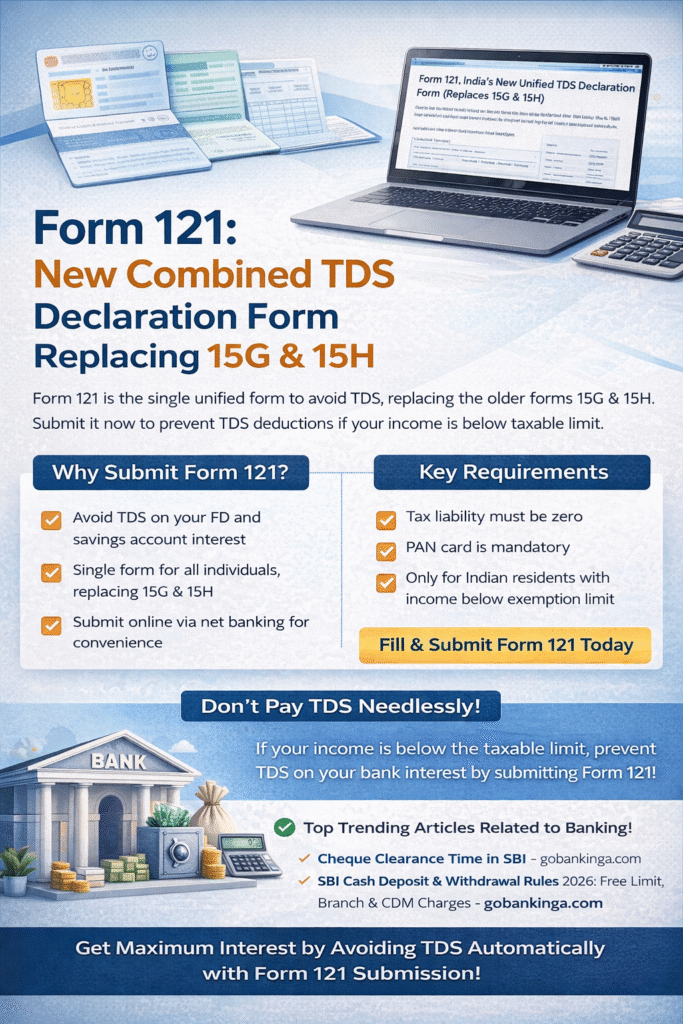

Simple meaning: If your tax liability is zero, you can submit this form to stop TDS deduction.

Example: If your total income is ₹2.5 lakh and FD interest is ₹40,000, your tax is zero. But bank may still deduct TDS. By submitting Form 121, you stop that deduction.

Who Can Submit Form 121?

| Category | Eligible | Condition |

| Individual (<60) | Yes | Income below limit |

| Senior Citizen | Yes | No tax liability |

| HUF | Yes | If eligible |

| Company/Firm | No | Not allowed |

| NRI | No | Not allowed |

You can now also check how to fill form 121 with a demo filled form.

When Should You Submit Form 121?

Best time is at the start of the financial year (April).

You can also submit before your interest is credited.

Late submission may lead to TDS deduction initially.

Key Conditions

| Condition | Details |

| Tax Liability | Must be zero |

| PAN | Mandatory |

| Resident | Indian resident |

| Income | Below exemption limit |

15G vs 15H vs 121

| Feature | 15G | 15H | 121 |

| Age | <60 | 60+ | All |

| Forms | Separate | Separate | Single |

| System | Old | Old | New |

Comparison

15G: For individuals below 60

15H: For senior citizens

121: One single form for all eligible categories

Why Banks Ask for Form 121

Banks are required to deduct TDS when your interest crosses a certain limit.

If you don’t submit Form 121, TDS will be deducted even if your income is below taxable limit.

By submitting this form, you inform the bank that your tax liability is zero.

Documents Required

– PAN Card

– Age proof

– Income details

– Bank account details

FAQ

1. Is Form 121 mandatory?

No, but required if you want to avoid TDS.

2. Are 15G and 15H discontinued?

They are being replaced by Form 121.

3. Can I submit it online?

Yes, through net banking in most banks.

4. What if I don’t submit it?

TDS will be deducted.

5. Does this mean no tax?

No, only TDS is avoided.

Pingback: Cheque Clearance Time in SBI - gobankings.com

Pingback: SBI Cash Deposit Charges Savings Account (2026): Free limit, Branch Rules & CDM Deposit Charges

Pingback: How to Fill Form 121 for Bank TDS Declaration – Easy Step-by-Step Guide